As we wrap up Black History Month, we must talk about policies that plague black Americans until this day—Redlining!

This sad story may make liberals and conservatives alike uneasy. But we all could use a little political humility these days, for good and evil can be found in unexpected places.

President Ronald Reagan said, “The nine most terrifying words in the English language are ‘I’m from the Government, and I’m here to help.’”1 If nothing else, this statement is surely true for generations of Black Americans victimized by the insidious redlining scheme most notably perpetrated by the Federal Housing Administration (FHA). Furthermore, this mandated racism infected other government programs and private commercial practices, thereby magnifying the harm.

With emancipation, a whole new train of troubles beset the newly freed. One among many was uninhabitable housing. The exploitive sharecropping system tied many to housing arrangements as bad or worse than slave quarters.2 Those who sought work in cities, north and south, endured dangerous and unhealthy slums. Yet government showed no interest in addressing Black housing inequities.3 There were, however, pockets of prosperous communities, both rural and urban, built by African Americans. Examples of these were the town of Rosewood, Fla., and neighborhoods of Atlanta and Tulsa, all three of which were destroyed by resentful white mobs.4

As we shall see, many surviving and thriving Black neighborhoods would be lawfully destroyed by the designs of 20th century “expert” federal planners.

The Origin of Racist Redlining

With the advent of the Great Depression and widespread homelessness, President Franklin Roosevelt’s New Deal, which was really trial-and-error, first sought to tackle the affordable housing shortage through the Public Works Administration (PWA). This agency was tasked with building new public housing and thus create construction jobs. Although originally planned for working-class whites, of the 47 strictly segregated projects, 17 were eventually allotted to Black families.5

Therefore, the federal government had, for the first time, offered permanent housing to low-income Black citizens, but in doing so, violated PWA policy against segregating races in neighborhoods not previously segregated. And, unlike the white projects, the PWA placed the African American projects in high poverty areas. Accordingly, segregation became federal practice regarding public housing.6 Nonetheless, the worst of New Deal housing management was to come with private housing.

For over a decade before the Depression, both Democratic and Republican administrations pursued policies to encourage single-family home ownership but met with little success. The average bank mortgage terms were simply out of reach for most of the middle-class: 50% down, interest only payments and full payment in five to seven years.7

Then the economic collapse and resulting joblessness crushed what housing market there was. Moreover, a tidal wave of foreclosures was sweeping away the homes and farms of those who had financed. With masses unable to pay loan payments or rent, homelessness skyrocketed, with evicted families living in tar paper camps called “Hoovervilles,” vehicles and under bridges, while the stressed and failing banks, having refused borrowers any forbearance, owned countless unoccupied, unmaintained and unsalable dwellings.8 In response, in 1933, the first year of his administration, the charismatic FDR won establishment of the Home Owners Loan Corporation (HOLC). The corporation bought mortgages near default and offered financing to new buyers. Repayment terms were from 15 to 25 years with payments including principal and interest. Hence, owners could realize equity in their mortgaged property.9

But HOLC evaluated danger of default before entering into an agreement. This included a house’s condition and the stability of surrounding property values. To make the task easier, HOLC concocted color-coded maps of America’s urban areas. The riskiest areas were red. This was called “redlining” even though the red areas were completely shaded. One Black person in an otherwise solidly white neighborhood rendered it red. In other words, being Black alone was enough to deem a person and those in their vicinity a bad risk. This created a new and mighty economic incentive for racism and segregation.10

The Democratic administration’s unfair housing policies perhaps overcame any hesitation because Black Americans were overwhelmingly Republican. Black loyalty to the GOP was rock-solid under 1920s Republican President Calvin Coolidge, who encouraged Black political participation, proposed making lynching a federal crime and urged federal investment in Black youth by educating more in the professions to economically lift their communities.11

Nevertheless, Coolidge’s less wise successor, President Herbert Hoover, deliberately drove Black leaders from the Republican Party in an unprincipled and unsuccessful attempt to attract southern white support.12 While most African Americans remained Republican during the early 1930s, their allegiance was weakening. And in the 1936 election, there was a colossal shift to the Democrats, for FDR’s always bold and often humanitarian New Deal agenda greatly aided desperate low-income Black families, despite countervailing and little-known redlining.13

Redlining Runs Rampant

To help new homebuyers obtain private bank financing, an even larger and more powerful New Deal agency was founded in 1934: the Federal Housing Administration (FHA). The FHA (now part of HUD) insured 20-year bank mortgages covering 80% of the purchase price. The agency conducted the risk appraisals, and its policy mandated a finding of “whites-only.” Using redlined maps, community racial segregation was required to receive indispensable FHA access.14

Racially mixed areas were also deemed too risky, as well as white borrowers in white areas near African American neighborhoods. However, a white neighborhood near a Black one could avoid risky status if a substantial physical barrier separated the two, such as a highway, wide boulevard, wall or deep concrete culvert. FHA guidelines also favored suburban over urban areas and the preservation of segregated public schools, justified as a means of maintaining racial harmony and property values.15

The impact of redlining widened tremendously when the FHA began underwriting whole subdivisions during the post-war housing boom and FHA policies were adopted by the wildly popular VA mortgage program. Consequently, redlining governed most housing construction in the United States.16

Redlining practices swiftly poisoned all sorts of other private commercial activities. For instance, FHA rules enticed realtors to fulfill redlining’s goal of protecting property values, and their commissions, with restrictive covenants in deeds and other legal documents to forbid the sale of homes to Blacks. These covenants preserved the segregation of neighborhoods far into the future and gave an excuse for refusing mortgages to Black applicants by public and private financial institutions.17

As for Black communities, redlining, the American antithesis of free enterprise capitalism, blocked investment and improvement by not only being applied to all residential mortgages, but also to home improvement, commercial construction and business loans and lines of credit. “Food deserts” arose as grocery chains would not or could not build stores. The same was true of other job producing businesses and suppliers of basic goods and services.18

Financial exclusion was only the beginning. Redlining instigated physical and psychological isolation as well. Expressways and other obstacles were erected to contain, divide or destroy traditionally Black neighborhoods. While being blamed for their plight, remaining residents were trapped in isolated red zones of poverty, decay, unemployment, crime, homelessness, hopelessness and fear. It became a perpetual economic death spiral outlasting redlining itself. In sum, redlining caused these problems by blocking investment, and these problems themselves, in turn, block investment to the present day.19

Some favorably situated Black communities were taken involuntarily through condemnation proceedings, then turned over to private investors. The homes were replaced by upscale apartment, condo, shopping, entertainment, recreation and sports complexes or gentrified and sold at considerable profit to the wealthy or young upwardly mobile outsiders, all in the name of progress or rejuvenation. These “slum clearance” endeavors were frequently and ironically funded by government bonds and federal “urban renewal” grants.20 In any event, the Black residents were gone. To make the developers and newcomers feel better, an inconspicuous marker might be installed to commemorate the site of a once historic Black neighborhood.

Legal Responses to Redlining and New Dangers

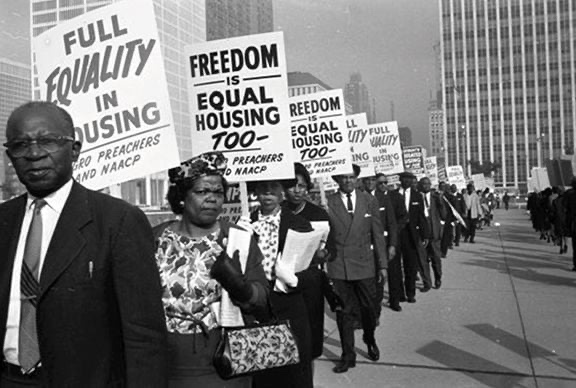

The United States Supreme Court made restrictive covenants unenforceable in the 1948 case of Shelley v. Kraemer.21 At last, after many protests, tireless lobbying and much legislative effort, the monumental Fair Housing Act of 1968, enthusiastically signed into law by President Lyndon Johnson, made it illegal for lenders to consider race in granting credit, but many banks continued to use redlining practices anyway. And as an alternative to now illegal redlining, and not to mention violent intimidation, zoning ordinances were increasingly employed following the same racist attitudes on protecting property values of white neighborhoods, while inflicting the same segregating harm on Black neighborhoods.22

Lawsuits under the new Fair Housing Act were not long in coming. In the landmark case of United States v. City of Black Jack23 (8th Cir. 1974), a religious nonprofit sought in 1969 to build a federally funded, racially integrated development of townhouses for low-income families in the unincorporated St. Louis suburb of Black Jack. White residents hurriedly incorporated and enacted zoning to ban new developments fitting the description of the townhouses and advocated on the old redlining prejudices.24

The Nixon administration responded with a fair housing suit. In 1974, after years of litigation, the appeals court held the zoning was racially motivated against Black citizens and ordered the municipality to allow construction.25 The precedent was made. Speaking of his administration’s varied and successful fair housing cases, Nixon said:

Denial of equal housing opportunity to a person because of race is wrong, and will not be tolerated….Not only have these suits directly opened to non-whites a great deal of housing previously available only to whites, they also have had a significant, wider impact in stimulating others to come into voluntary compliance with the anti-discrimination laws. This vigorous enforcement as required by law will continue.26

The same year as the Black Jack decision, over considerable opposition, President Nixon achieved enactment of the Legal Services Corporation (LSC) Act of 1974 federally funding legal aid organizations, and legal aid lawyers became an important part of Fair Housing Act enforcement supported by HUD grants.27 Finally, covert but pervasive private bank redlining was unequivocally outlawed and deterred by the Home Mortgage Disclosure Act (HMDA) of 1975 and the Community Reinvestment Act (CRA) of 1977.28

With victories came new dangers as new forms of housing discrimination emerged. One born in the 1990s was “reverse redlining,” a form of predatory lending whereby instead of excluding Blacks from housing, financing ensnared them in abusive loans. African American targets were first-time buyers unable to qualify for the prime market, those seeking to refinance and seniors with paid-for houses needing home improvements. The strategy was to lure the financially unsophisticated and elderly into subprime market loans with outrageous interest rates, purposely confusing terms, hidden balloon payments and extreme penalties setting them up for default. The result was record foreclosures on Black homes at the end of the first decade of the 21st century. Elderly, low-income homeowners simply needing money for siding or a wheelchair ramp were left homeless.29

In the vein of reverse redlining, there are the fine print rent-to-own traps aimed at low-income African Americans trying to become homeowners. These deals rarely end with ownership and normally provide for a much above market rent rate with the so-called tenant-buyer paying for repairs, improvements and taxes. Without notice, the adhesion contracts commonly convert to a simple rental upon a one-day late payment or some other seemingly minor event. Snap! The trap has sprung. The prey only learns of the change decades later when requesting a deed. The predatory slum lord “seller” wins the windfall and all the improvements the “buyer” made believing the house would one day be theirs. The disappointed victim leaves or is evicted. It is then time to again post the “For Sale” sign.

It is unknown what other novel ways of housing discrimination and race-based scams will be devised on the poor and elderly based on the living legacy of redlining. What is certain is what a member of Parliament said of Britain’s unjust policies against the American colonists is true of redlining and its progeny: They are “full of evil.”30 |||[Source]